Trump tariffs struck down, Strait of Hormuz disrupted, USMCA under review, and 3,000+ new trade measures in 2025. Here is the complete picture of global trade in 2026.

Global Trade in March 2026: Five Crises Every Importer Is Navigating Right Now

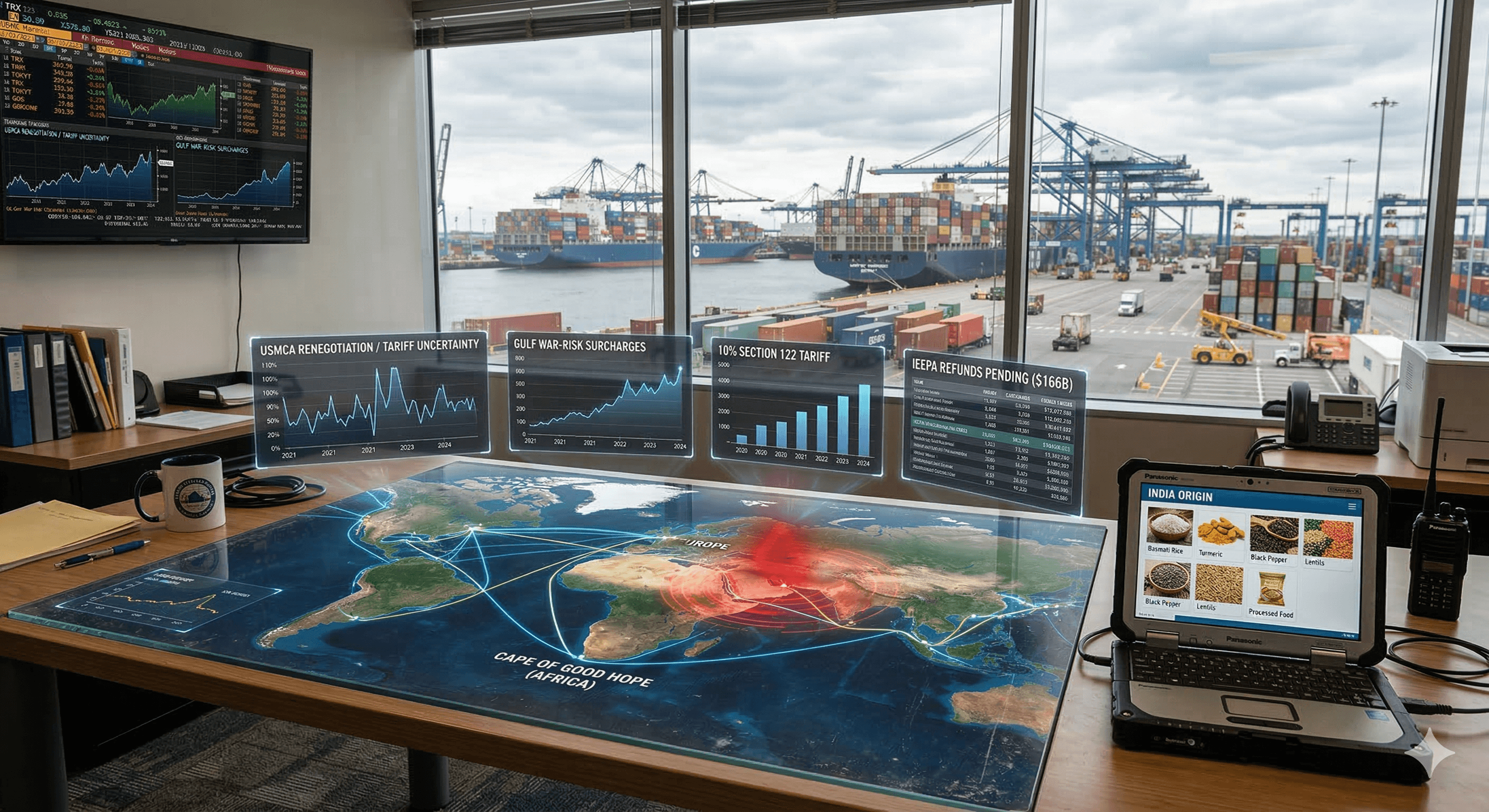

There has never been a more complex moment to be running an import-dependent business. In the first three months of 2026 alone, the US Supreme Court struck down the sweeping IEEPA tariffs that had reshaped global sourcing for the past year, a new 10% global tariff was signed into law under Section 122, the Strait of Hormuz was effectively closed after US and Israeli strikes on Iran, the USMCA free trade agreement entered active renegotiation, and more than 3,000 new global trade policy measures were logged globally in 2025 - more than three times the annual level recorded a decade ago.

For importers trying to plan supply chains, negotiate supplier contracts, and forecast landed costs, this environment is genuinely without precedent in the modern era. The businesses that will come through it strongest are the ones who understand what is actually happening, not just what was happening six months ago.

This blog breaks down the five most consequential developments shaping global trade in 2026 - and what each one means for procurement teams right now.

1. The US Tariff Situation ~ Chaos, Courts, and What Comes Next

The single most consequential development for global importers in early 2026 has been the US Supreme Court’s February 20 ruling that the International Emergency Economic Powers Act does not authorize the president to impose tariffs. In a 6-3 decision, the Court struck down the sweeping IEEPA tariff framework that had been the foundation of US trade policy for the past year.

The ruling didn’t eliminate US tariffs. It eliminated one legal mechanism used to impose them - and the Trump administration moved immediately to replace it. On the same day as the Supreme Court ruling, President Trump signed an executive order imposing a 10% tariff on all countries under Section 122, citing large and persistent US balance-of-payments deficits. The Section 122 tariff applies to approximately $1.2 trillion worth of imports after exemptions - and 24 states filed a lawsuit in the Court of International Trade to block it within two weeks.

The practical situation for importers as of mid-March 2026: the average effective tariff rate on US imports was 10.3% through January 2026, with China facing the highest rate at 33.9%. The replacement of IEEPA tariffs with the new 10% Section 122 global tariff is projected to lower the effective rate slightly to 7.7%. But the legal uncertainty is unresolved - the government’s system for processing IEEPA tariff refunds is only 40% to 80% complete, with $166 billion in payments awaiting refund processing.

For importers who paid IEEPA tariffs, the refund process is real but slow. For importers planning new shipments, the Section 122 tariff is in effect - until the courts say otherwise. The lesson is that US tariff policy 2026 requires active, weekly monitoring rather than quarterly planning cycles. The landscape is shifting faster than annual procurement reviews can track. On March 11, the USTR initiated new Section 301 investigations targeting China, the EU, Singapore, Switzerland, India, Vietnam, Bangladesh, and a dozen other countries, investigating structural excess capacity in manufacturing sectors. These investigations could pave the way to reimpose tariffs equivalent to what was struck down. The tariff story is not over - it has simply moved to a new legal arena.

2. The Middle East Conflict ~ Energy, Shipping, and Second-Order Effects

The US and Israeli strikes on Iran on February 28 triggered the most significant **global supply chain disruption** since COVID-19. The Strait of Hormuz - through which approximately 20% of global seaborne oil and a similar share of LNG normally transit - was effectively closed within 48 hours. Brent crude rose as much as 13% in early trading on March 2, briefly above $82 a barrel, as traders reacted to disrupted flows from the Gulf.

Every major shipping line suspended Gulf operations. MSC declared end of voyage for Gulf-bound cargo. Maersk, Hapag-Lloyd, and CMA CGM rerouted vessels around the Cape of Good Hope, adding 7 to 14 days to Asia-Europe transit times. Jebel Ali - the world’s largest man-made port - temporarily suspended operations after drone strikes caused a fire at its berths.

The oil price impact on trade has been partially cushioned by pre-built strategic reserves - China has approximately one billion barrels in storage - and by the US’s position as the world’s largest crude producer. Markets are currently pricing a short-duration conflict. Goldman Sachs models suggest Brent could climb a further $10 to $15 per barrel if the Strait remains disrupted for a full month with no offsets. For importers, the second-order effects matter as much as the headline oil price. Every shipping route that previously ran through or near the Gulf has been extended. War-risk surcharges and emergency conflict surcharges are now standard on affected lanes. Air freight capacity dropped 18% globally as Gulf airspace closed. And fertilizer prices are rising as natural gas from Qatar - the primary feedstock for nitrogen fertilizer - faces sustained supply disruption.

3. The USMCA Renegotiation ~ A $1.3 Trillion Trade Framework Under Review

The United States-Mexico-Canada Agreement is scheduled for renegotiation in 2026, and formal talks between US and Mexican negotiators began the week of March 16. The agreement currently enables about 90% of goods crossing the borders of the three countries to do so tariff-free - and if the US, Canada, and Mexico are unable to renegotiate and ratify the treaty, USMCA would be in limbo for ten years, subject to annual reviews.

The worst-case scenario - one or more countries pulling out of the agreement entirely - would eliminate USMCA tariff exemptions and expose approximately $1.3 trillion in North American trade to general tariff rates. For importers with North American supply chains, this is not an abstract risk. The US-Canada tariff conflict of 2025 demonstrated how quickly a previously stable trade relationship can fracture when political conditions shift.

The USMCA renegotiation also intersects directly with the broader US tariff agenda. The share of imports from Canada and Mexico claiming USMCA exemptions surged to nearly 85% in January 2026, meaning the agreement’s tariff protections are the primary reason Canadian and Mexican goods face effective tariff rates under 5% despite the broader tariff environment. Any weakening of those protections in negotiation would immediately raise costs for US manufacturers and retailers with North American supply chains.

For importers sourcing from outside North America - including those building Indian supply chains - USMCA uncertainty is both a risk and an opportunity. If North American supply chains face higher costs from a weakened USMCA, the relative competitiveness of Indian-origin supply improves further.

4. The Global Trade Policy Fragmentation ~ 3,000 New Measures in One Year

Beyond the headline US tariff story, the broader global trade fragmentation trend is running at a pace that most procurement teams haven’t fully internalized. More than 3,000 new trade and industrial policy measures were introduced globally in 2025 - more than three times the annual level recorded a decade ago.

These measures are not just tariffs. They include export controls on critical minerals, non-tariff barriers in food safety and labeling, local content requirements, import licensing regimes, and bilateral trade restrictions driven by geopolitical alignment rather than economic logic. Governments are expected to continue using tariffs as protectionist and strategic tools in 2026, with tariff use rising sharply in manufacturing sectors.

The impact on supply chain planning is structural. Global value chains continue to shift as firms move away from cost-driven offshoring toward risk management, with geopolitical tensions, industrial policy, and technological change driving supplier diversification. The companies that built supply chains purely on lowest-cost logic in the 2000s and 2010s are now bearing the cost of that approach - repeatedly.

The supply chain diversification imperative is not a buzzword anymore. It is a measurable competitive advantage. Companies with sourcing relationships across multiple geographies, multiple carrier relationships, and inventory buffers calibrated to disruption rather than just-in-time efficiency are absorbing these shocks materially better than those without that architecture.

For food importers specifically, the agricultural trade environment carries its own pressures. Food and agricultural products account for around one third of commodity exports, with conflicts, trade restrictions, and extreme weather continuing to disrupt supply. Fertilizer prices surged in 2025 and remain high, raising production costs. Keeping food trade open and maintaining diversified origins is more urgent than it has been at any point in the past two decades.

5. The Resilience Economy ~ How Leading Importers Are Responding

Against this backdrop of simultaneous disruptions, the most important development in importer supply chain strategy is the decisive shift toward resilience as a business priority. Nearly three in four business leaders now prioritize resilience investments, with 74% viewing resilience as a driver of growth rather than a cost.

That shift is showing up in concrete procurement decisions. Companies are building longer inventory buffers - moving from 30-day to 60 or 90-day stock positions for critical inputs. They are qualifying multiple suppliers across different origins for the same product category, accepting a small cost premium for the redundancy. They are investing in visibility systems that give them real-time shipment status rather than learning about delays after they’ve already affected customers. And they are writing force majeure and alternative routing clauses into supplier contracts rather than assuming standard terms will cover novel disruption scenarios.

Global economic growth is projected to hold steady at 3.3% in 2026 - an upward revision from October estimates - reflecting surprising resilience despite the tariff shock. The headline number masks significant divergence underneath: the US is projected to slow to 1.5% growth, Europe is struggling with demand, and developing economies excluding China are slowing to 4.2%. For importers, slower growth in key markets means margin pressure from both the cost side - tariffs, freight, energy - and the revenue side - softer consumer demand.

Smaller, less diversified economies are most exposed to global trade disruption, with limited capacity to absorb higher costs or redirect exports. For importers sourcing from developing country origins - including India - understanding which of your suppliers have the financial and operational resilience to absorb these shocks matters. An exporter who cannot maintain quality standards, certification compliance, or delivery commitments under supply chain pressure is a risk that lands on the importer’s balance sheet.

What This Means for India as a Sourcing Origin

India’s position in this environment is genuinely distinctive. It is not in a trade war with the United States - the February 2026 US-India trade deal reduced tariffs on Indian goods from 50% to 18%, and Indian agricultural products including spices received specific tariff exemptions. It is not party to the Middle East conflict - Indian ports are fully operational and India-origin shipments on Cape of Good Hope routing were already normalized after the 2023-2024 Red Sea crisis. The India-EU FTA signed in January 2026 is improving the landed cost picture for European buyers progressively over its implementation timeline.

India is not immune to the disruptions described in this blog. Rising LNG prices affect Indian fertilizer costs. Global freight rate increases affect Indian export logistics. But relative to the alternatives - Chinese origins facing 33.9% effective US tariffs, North American supply chains exposed to USMCA uncertainty, Gulf-region supply chains directly inside the current conflict zone - India’s trade stability is a genuine structural advantage for importers who are rethinking their sourcing geography.

At Bayharbor Exports, we supply basmati rice, spices, lentils, and processed foods from India to markets across the US, Europe, the Middle East, and beyond. Our operations are unaffected by the current Gulf crisis, our documentation infrastructure is built for compliance in demanding markets, and our logistics partnerships are adapted to current routing realities. If the global trade picture outlined in this blog is prompting a rethink of your sourcing strategy, we are ready to have that conversation.

Our blog on [how the US-Canada food trade war is reshaping importer supply chains](#) covers the North American sourcing disruption in detail. Our [complete guide for European importers on the India-EU FTA](#) walks through what the January 2026 agreement means in practice for EU buyers.

Frequently Asked Questions

What happened to the Trump IEEPA tariffs in February 2026?

Is the 10% Section 122 tariff currently in effect?

How is the Middle East conflict affecting global shipping right now?

What is the USMCA renegotiation and what are the risks for importers?

Why is India considered a stable sourcing origin in the current environment?

What should importers be doing right now to manage the current trade environment?

The Bottom Line

Global trade disruption in 2026 is not a single event - it is a simultaneous cluster of crises that intersect and amplify each other. US tariff policy is in legal flux. The Strait of Hormuz is disrupted. USMCA is under active renegotiation. Three thousand new trade measures entered force globally last year. And all of this is happening while global growth slows and margin pressure tightens.

The importers navigating this best are those who accepted two years ago that the era of stable, optimized, just-in-time supply chains was over - and invested in resilience accordingly. The importers struggling most are those still hoping for a return to the pre-2025 normal that is not coming back.

Diversification, visibility, and supplier quality discipline are not optional features of a mature procurement operation anymore. They are the baseline requirements for operating in the environment that now exists.